Download the PDF

Despite a growing economy and low unemployment, state general revenue has dropped significantly, hindering the ability of Missouri to invest in the resources our communities need to prosper. State revenue trends generally reflect economic indicators. However, external factors like costly corporate tax changes and the implementation of Kansas-like tax policies have contributed to Missouri’s stagnant state revenue growth.

These changes come on top of two dozen tax changes over the last two decades. When Missouri’s 2014 Kansas-like tax cuts are fully phased in, they will further limit Missouri’s ability to invest in the education, job training, health, child welfare, infrastructure, and other resources our state needs to grow its economy, and Missouri families need to provide a better future for their families.

Current Year State General Revenue Does Not Reflect State’s Economic Growth

Other Factors Like Tax Changes Impeding Revenue

Missouri is in a period of relative prosperity, with a growing economy and high employment. In fact, as of March, Missouri’s unemployment rate was just 3.6 percent – the lowest unemployment rate since 2000.

Normally, state revenue trends would reflect that economic growth. Instead, state general revenue in Missouri continues to struggle and hinder the ability of Missouri to invest in the community services that provide the foundation for families and the economy to thrive:

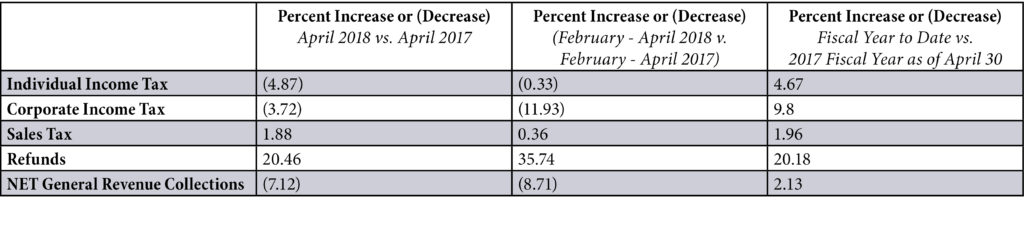

- State general revenue dropped by 7.1 percent net of refunds in April compared to April of 2017.

- For the 2018 fiscal year to date, the April decline results in a net growth for the year of 2.1 percent compared to the previous fiscal year.

The amount of revenue growth for the year is well below the original revenue estimate of 3.8 percent, which is what the current year’s budget was based on. However, the Governor withheld $251 million in appropriations at the start of fiscal year 2018, and state lawmakers revised the revenue estimate downward to 1.9 percent. As a result of these changes, revenue is likely to reach the revised estimate, but it will not allow for releases of the withheld appropriations, which impacted an array of community services including health, mental health, local schools and colleges.

Trends over the last three months of the year (February to April) indicate that the drop in revenue is likely directly tied to recent state tax changes.

- In January, Missouri began the phased-in implementation of the Senate Bill 509 tax cuts (approved in 2014).

- The Senate Bill 509 cuts are expected to reduce state revenue by $150 million in the first tax year of implementation. When fully phased-in over the next several years, the bill will reduce state revenue by $720 million per year.

*This table shows major categories of general revenue only. For more detail on all categories of general revenue see Missouri Office of Administration, Division of Budget & Planning, Monthly Revenue Reports for the Current Year by Month

*This table shows major categories of general revenue only. For more detail on all categories of general revenue see Missouri Office of Administration, Division of Budget & Planning, Monthly Revenue Reports for the Current Year by Month

Missouri is at Historic Lows

Missouri’s decline in revenue is not merely a short-term dynamic.

One common way to evaluate state general revenue from a histroric context is to measure net general revenue as a percent of the economy – or total personal income in the state – over time.

- Using this metric, Missouri’s ability to fund community services through general revenue dollars has dropped significantly

by historical standards.

by historical standards.

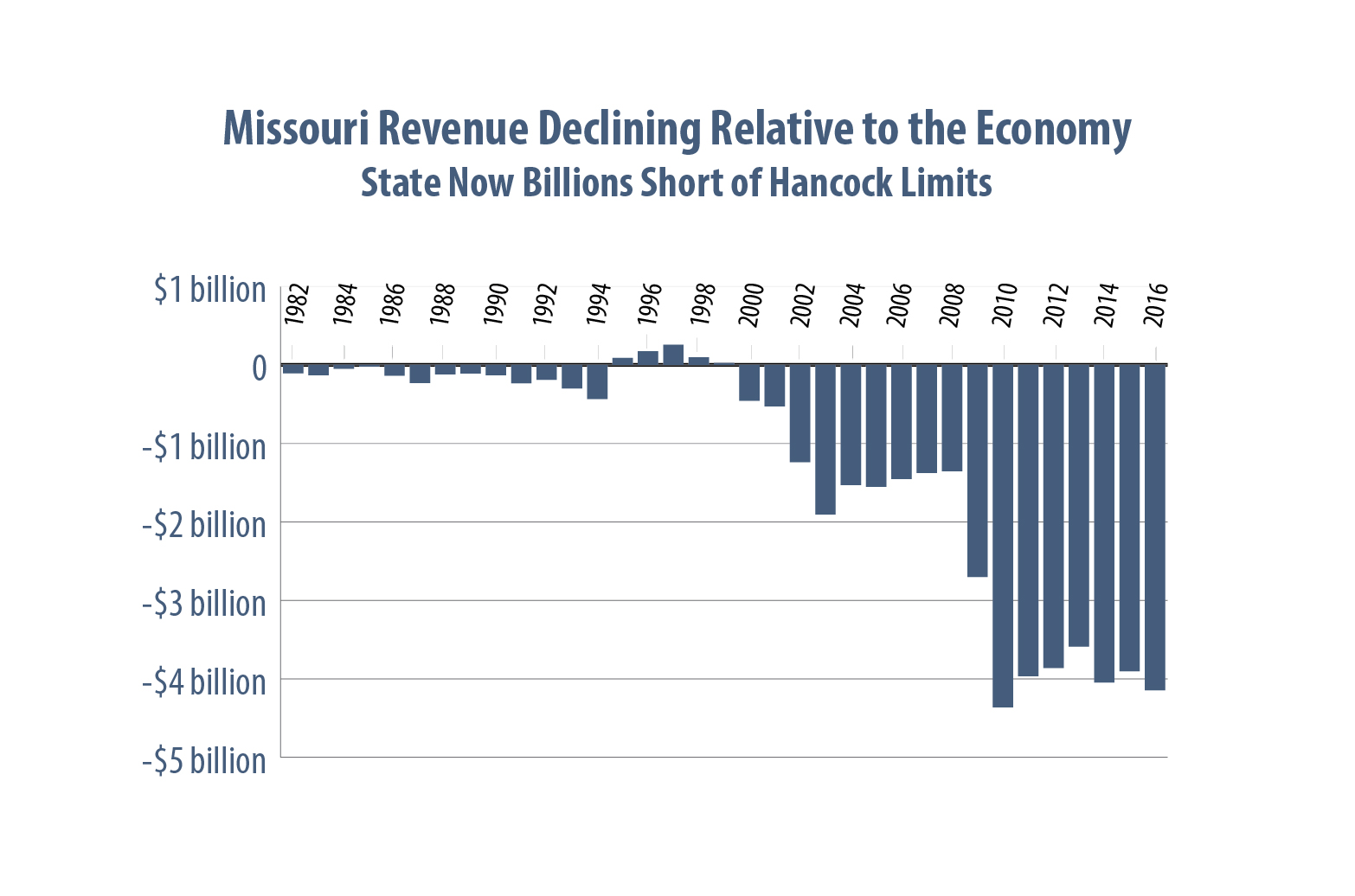

The table shows general revenue as a percent of personal income from state fiscal year 1981 through 2017.

- General revenue peaked in 1997, but has fallen steeply since that time.

- Although it edged up modestly since the recession, state general revenue as a percent of personal income in Missouri remains below 1981 levels.

For context, if general revenue had maintained the year 2000 ratio of 4 percent of state personal income, Missouri would have had about $1.5 billion more in available revenue for the 2017 state budget.

Missouri and the“Hancock Lid”

Another barometer for Missouri’s revenue trends is the state’s “Hancock lid” – a provision in Missouri’s state constitution that restricts the growth of state revenue to the ratio of personal income that it comprised in 1980.

- Missouri revenue did not reach this limit until the late 1990s, when economic growth was exceptional.

- From 1995 to 2000, the state reached the lid every year and was required to refund nearly $1 billion to taxpayers.

- Though a significant amount of money as a whole, the average Missouri family received a refund of just $40 over those five years.

- Unfortunately, lawmakers started to believe Missouri was flush with money, and that the state needed to cut taxes to avoid the Hancock lid.

In fact, between 1993 and 2013, state lawmakers passed 20 different tax cuts, which combined cost more than $1 billion per year. While some of these cuts benefitted families, many were targeted to corporations, including a phase out of the corporate franchise tax and changes to the ways corporations can determine what profits are taxed.

As a result, Missouri is now $4.146 billion below the Hancock lid. By nearly every measure, Missouri invests less in critical public services today than it did nearly three decades ago.

Missouri Today: Fundamental Services Eroded

Missouri is now unable to fund the very public services that allow our families, communities, and economy to thrive, like education, public health, public safety, & transportation.

- Not only have services been cut over the last decade, but each year they compete against each other for more limited increases.

- Services for our grandparents have been pitted against services for our children, and health services for our neighbors living with disabilities have been pitted against other financial supports that help seniors and people with disabilities remain independent in their own homes.

Missouri Tomorrow: The Pending Cliff

Unfortunately, without intervention, Missouri will struggle more and more to meet the needs of its residents.

In 2014, state lawmakers passed Senate Bill 509, an unaffordable tax cut package that will reduce state general revenue by an additional $720 million per year when fully implemented. The cuts are being phased-in incrementally beginning in 2018 and include two major provisions:

- A 0.5 percent reduction in the top individual income tax rate, reducing it from 6 to 5.5 percent

- A new 25 percent tax deduction for businesses that file their taxes through the individual income tax, which includes LLCs, sole proprietorships, and partnerships (like lobbyists, for example)

All Missourians will be negatively impacted by the reduction in services forced by the tax cut.

But the tax benefits of the bill disproportionately go to wealthy Missourians.

Missouri cannot afford more short-sighted tax changes that will hinder our communities.

Without the resources needed for our pre-K to 12 classrooms, higher education & job training, roads & bridges, and more, Missouri families will be left to pay the price.